A commonly cited estimate in the financial industry is that Baby Boomers will pass down $68 trillion to their children—providing the Millennial population with five times as much wealth in 2030 as it has today.

However, some financial experts argue that current economic conditions, ranging from skyrocketing housing prices to rising elderly healthcare costs, will shape how much, when, and how Baby Boomers will pass down these inheritances.

So, what does this mean for the Millennial recipients?

Housing Costs Cut Inheritance Timelines

One trend experts notice is that many Baby Boomers are transferring inheritances in their lifetimes versus on their way out.

“More and more of my clients who are nearing retirement, part of that Baby Boomer generation, are starting to step in and help their adult children gain access to the housing market,” said James Ciprich, partner and wealth advisor at Corient, an investment firm managing $149 billion for private clients. “The motivation is clear: They want to help their children buy their first home or even buy it for them in a real estate market that has been out of reach for the past few decades.”

Besides the cost of home values, which have increased more than 87% from July 2008 to July 2023, according to the S&P Case Shiller Index by the St. Louis Fed, rising interest rates also add to the home-buying conundrum.

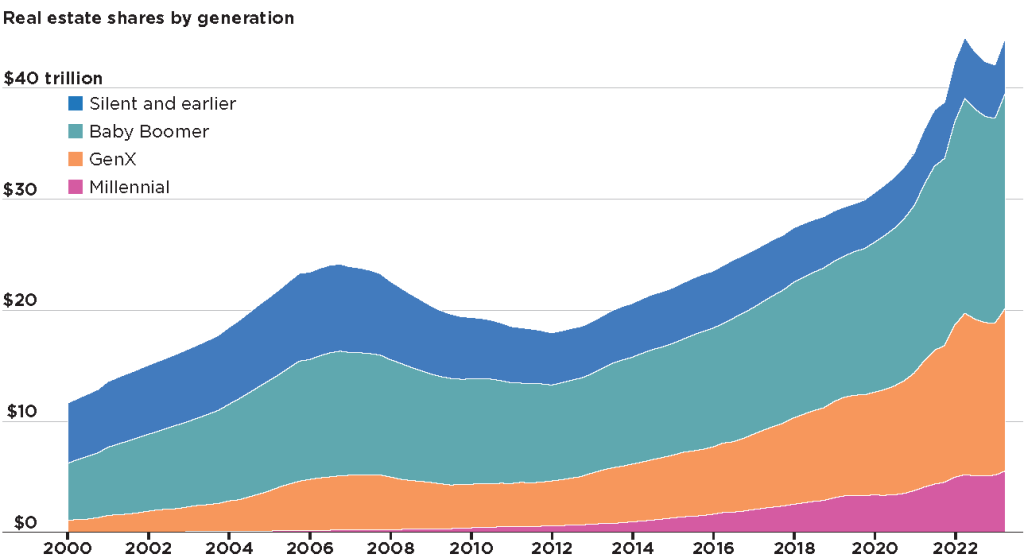

Federal Reserve data also points to how Millennials haven’t been able to gain a significant share of the U.S. real estate market in the last 15 years. As of Q2, 2023, Millennials own just 12.4% of the real estate market, vs. 43.5% for Baby Boomers. (Boomer’s share hasn’t changed much from fifteen years ago, when it was 47.4% of the market.)

When asked how they wish to spend their inheritances, Millennials also share a fiscally responsible vision like their parents.

“I do have an inheritance in my parent’s real estate business, and my first priority is to ensure financial stability,” says Benedict Ang, a professional MMA fighter and senior coach at Total Shape, an Indiana-based fitness website. “I’ll invest thoughtfully, diversifying my portfolio and maintaining a financial cushion for unexpected expenses.”

Ang also mentions that he, like his parents, wants to give back much of that inheritance to philanthropic causes and continue building on his parent’s legacy.

Tax Changes Spur Earlier Giving

Another element that will shorten the timeline of wealth transfer is the tax environment. Five years ago, President Donald Trump signed The Tax Cuts and Jobs Act of 2017 into law, providing eight years of estate and gift tax relief through an elevated exemption of $12.92 million per individual and $25.84 million for married couples. However, The Tax Cuts and Jobs Act will expire in 2025, cutting these exemptions in half unless Congress enacts new provisions.

“This looming change in tax legislation may motivate Baby Boomers to make sizable gifts to take advantage of the current exemptions,” Ciprich states.

In addition to passing down an estate, Ciprich sees many of his clients passing down annual cash gifts to their Millennial children and taking advantage of so-called 529 accounts. You can pass these investment accounts to future generations, who can use them for qualified education expenses such as higher education.

According to current estate and gift tax guidelines, you can give up to $17,000 a year, or $34,000 if you’re a married couple, to as many individuals as you wish. But as far as 529s are concerned, singles can give up to $85,000 in a single year, and married couples $170,000, where the money will grow tax-free for years to come.

Tax laws incentivize earlier giving, and Ciprich states that retirees should generally consider gifting in their lifetime for reasons such as helping their children start a business or buy a home. Waiting 10-15 years to receive inheritances might mean Millennials miss out on time-sensitive business and housing opportunities.

There’s a danger, in fact, in holding on to too much money. “The decision comes down to whether their estate will grow to the point where it exposes them to federal and state taxes,” Ciprich says. “In these situations, they prioritize family and charities over the government.”

Experts say that it’s rare that many individuals will have to pay any estate tax to the IRS, especially if they fall below the $12.92 and $25.84 million exemptions for individuals and married couples. Retirees will, however, have to pay attention to their respective states to see if they live in one of seventeen with estate or inheritance taxes. These states include Washington, Oregon, Minnesota, Illinois, New York, and New Jersey.

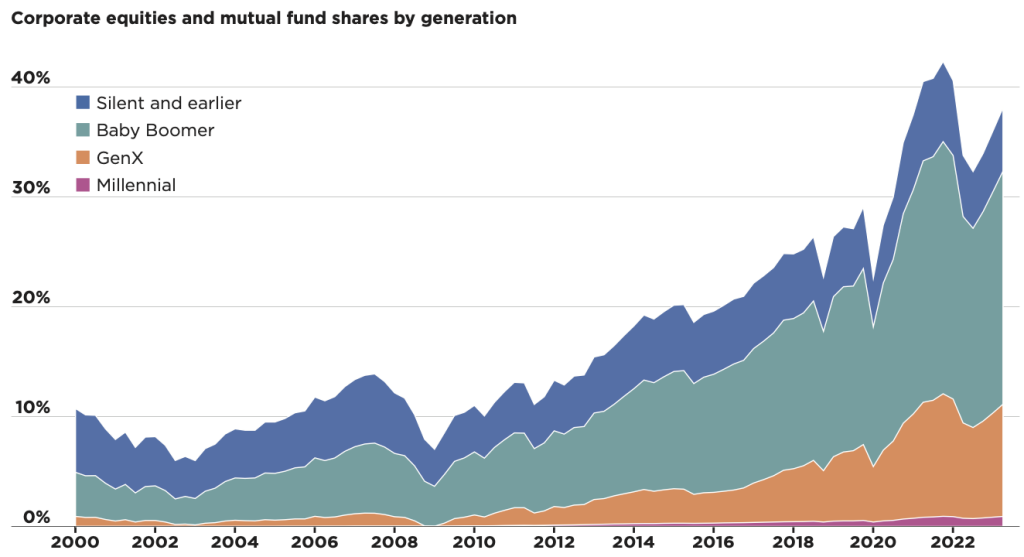

Baby Boomers Still Own Lion’s Share of Stocks /

Source: Federal Reserve

Choosing Between Legacies and Healthcare

While some Boomers pass down properties to their Millennial children, one expert argues that rising long-term healthcare costs may take away even the possibility.

“Waves coming of Baby Boomers find themselves in a position where their largest asset is their home, and they have to figure out how to cover their cost of aging,” said Laurie Allen, CFP, owner of LA Wealth Management, a firm advising both Baby Boomers and Millennial clients. “Some homes must be sold to cover ongoing costs.”

“Another element that will shorten the timeline of wealth transfer is the tax environment…The Tax Cuts and Jobs Act will

expire in 2025, cutting these exemptions in half.”

The California market, where Allen’s office resides, saw that nearly half (49%) of Californians skipped or postponed some type of health care, such as visiting their doctor, dentist or home care, in the last 12 months due to cost. But it’s not just California, as 22% of those 65 and older, according to Kaiser Family Foundation, will forgo medical treatment due to skyrocketing costs. This means fewer dollars to pass down to their children.

Allen’s advice to Millennial children and parents is simple: protect your inheritance and opt for long-term care insurance through an external provider. Long-term health insurance covers assistance for activities such as, but not limited to, bathing, transportation, and eating that some people may no longer be able to do.

“When I bring up long-term care for my clients 50 and older, many people scoff at the price and say they don’t want to pay $200-$300 a month,” Allen says, referring to insurance premiums. “But I tell Millennials, if it’s affordable for you, take care of your parent’s long-term health care so you can protect your assets.”

It’s worth noting that more than half of American boomers believe Medicare will cover their long-term healthcare costs, which is inaccurate, according to a recent study by Banker’s Life, an insurance and retirement solutions provider.

Medicare only covers care after hospitalization, and supplement plans will have limited coverage for food delivery and transportation to medical visits. Retirees cannot tap into Medicaid, which is meant for low-income Americans unless they’ve depleted their savings. They must explore options from an insurance marketplace, agents, or their current employer.

Rising Living Costs Shrink Inheritances

Experts also predict the high cost of living may reduce much of the investment inheritances Millennials expect to receive. Some Millennials may not get a substantial multi-million dollar inheritance slice; they may simply get their parent’s home or none of the above.

“I see two stories: One involves a Baby Boomer parent who was fortunate enough to buy property when it was more affordable where, thanks to the significant appreciation in property values, they’ve left behind a substantial inheritance, even if they didn’t have much else to pass on,” Allen states. “If they own a mortgage-free home worth $1.2 million or more, it’s a substantial inheritance. They can potentially avoid significant taxes by placing the home in a trust.”

Allen then points out that the other story we may see is Baby Boomers passing down their investments through a trust.

“If parents were savvy enough to save earlier, they’re passing on investments in addition to homes through a trust and making sure appropriate beneficiaries are named,” Allens says.

Like the real estate numbers, Baby Boomers’ stock market shares haven’t shifted much in the last decade and a half. While the older generation’s portfolios continue to grow, their children’s lag.

According to the Federal Reserve, in 2008, Baby Boomers retained 48.1% of these investments, only 7.6% behind what Baby Boomers own today. In 2023, Millennials straggle far behind at only 2.4%.

Overall, the wealth transfer from Baby Boomers to younger generations is a macro-trend that will shape the future of financial and economic landscapes.

The changing attitudes of Baby Boomers towards wealth transfer, focusing on lifetime gifting and meaningful spending, will shape how much their wealth is transferred to younger generations. But ultimately, people will only know exactly how this $68 trillion is shared and how much once decades have passed.